SUMMARY

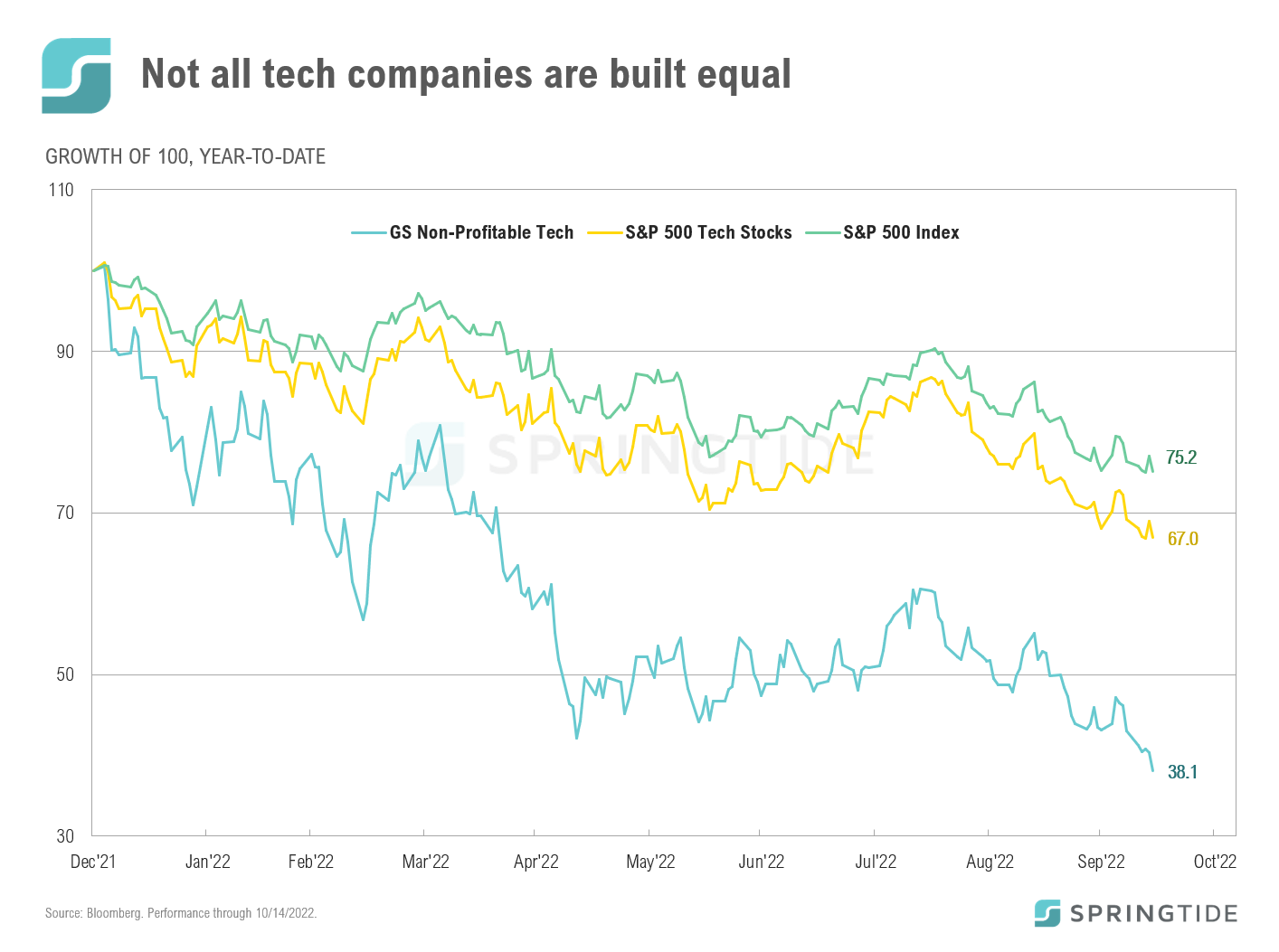

- Like most bear market environments, 2022 has seen growth stocks materially underperform their value counterparts. Of the growth stocks, tech has been among the hardest hit, with the S&P 500 tech sector down 33% year to date — trailing the broader index by over 8.0%. One of the key contributors to the underperformance of growth, and tech, has been the sharp rise in interest rates over the year.

- One way of calculating the fair value of a company is by discounting all future cash flows to their present value. Therefore, when interest rates rise, future cash flows become less valuable as they are discounted at a higher rate due to the increased opportunity cost.

- The timing of cash flows can also exacerbate the effect of higher discount rates as cash flows further out are discounted for a longer period relative to near term cash flows. For example, non-profitable companies which are only expected to start generating cash flows several years down the line are more impacted by discount rates than profitable companies with stable cash flows. This can be evidenced in the year-to-date performance of non-profitable tech companies, which (as proxied by the Goldman Sachs Non-Profitable Tech Index) has lost -61.9% year to date — almost 19.1% more than S&P 500 tech stocks. The longer the high interest rate environment persists, the more headwinds non-profitable businesses will face.

DISCLOSURES

The material shown is for informational purposes only. Any opinions expressed are current only as of the time made and are subject to change without notice. This report may include estimates, projections or other forward-looking statements; however, forward-looking statements are subject to numerous assumptions, risks, and uncertainties, and actual results may differ materially from those anticipated in forward-looking statements. As a practical matter, no entity is able to accurately and consistently predict future market activities. Additionally, please be aware that past performance is not a guide to the future performance of any investment, and that the performance results and historical information provided displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, it should not be inferred that these results are indicative of the future performance of any strategy, index, fund, manager or group of managers. The graphs and tables making up this report have been based on unaudited, third-party data and performance information provided to us by one or more commercial databases. While we believe this information to be reliable, SpringTide Partners bears no responsibility whatsoever for any errors or omissions.

Index benchmarks contained in this report are provided so that performance can be compared with the performance of well-known and widely recognized indices. Index results assume the re-investment of all dividends and interest. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. This presentation is not meant as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s accounts should or would be handled, as appropriate investment decisions depend upon the client’s specific investment objectives.

SpringTide Partners, LLC is a registered investment adviser with the Securities and Exchange Commission; registration does not imply a certain level of skill or training. For more detail, including information about SpringTide’s business practices and conflicts identified, please refer to SpringTide Partners’ Form ADV Part 2a and Form CRS at: https://www.springtide-partners.com/disclosures